IRS enforcement has cooled in the years following the COVID-19 pandemic, but the 2022 Inflation Reduction Act is equipping the agency with over $45 billion for tax enforcement. With high interest rates in place, now is an even worse time to owe the IRS. Here is an overview of back taxes and how to get rid of them.

What are back taxes?

Back taxes are unpaid taxes from a previous year. For example, if you had a tax bill of $1,000 after filing your 2021 tax return and did not pay it, you owe back taxes. Not only would you owe the $1,000, but you would also owe any penalties and interest that accrued on this tax bill. You can owe taxes by not reporting all earned income, not filing a return, or filing but failing to pay your tax bill.

What happens if I don’t pay back taxes?

Unpaid taxes will result in an IRS notice, which is a formal letter from the IRS. Typically, the notice will advise the taxpayer to pay the balance owed within 21 days. If the balance is still unpaid within 60 days, the IRS will likely proceed with collections. While the IRS is awaiting payment, the tax balance will accrue interest and penalties.

How do I get rid of back taxes?

If you do find yourself in the unfortunate situation of owing the IRS, there are some options for how to pay your back taxes. If you cannot afford to pay, you still have options. It’s important to know that there are always options and the worst thing you can do is ignore the issue.

Pay your taxes

This is the most straight-forward solution to getting rid of back taxes. If you can afford to pay off your tax balance, you should do it immediately to avoid additional penalties and interest. IRS interest rates are high right now, making your tax bill more expensive than it would’ve been in previous years. You can pay your tax bill with a credit or debit card through your online IRS account, by phone or even on the IRS mobile app. If you don’t have enough to cover the balance, you can request a short 120-day extension with the IRS. This option doesn’t stop interest or penalty fees, but it will allow more time to pay the tax debt in full. Even borrowing from your retirement fund or taking out a personal loan might be a better option than allowing your tax balance to grow.

Request an Installment Agreement

You can request an installment agreement, or a monthly payment plan, with the IRS. With this option, the 0.5% monthly penalty will be reduced to 0.25% until the balance is paid off. Interest will continue to accrue until the balance is paid. If you cannot pay your back taxes within 120 days and you owe less than $50,000, this might be the best option for you. Taxpayers should note if they do not pay according to the IRS’s set schedule, they can void the installment agreement and proceed with enforcement.

Apply for an Offer in Compromise

In some cases, the IRS may settle your tax debt for less than the amount you owe with an offer in compromise (OIC). This is understandably the most sought-after option to get rid of back taxes, but it is also rarely approved by the IRS. To qualify, taxpayers need to prove that paying off their tax debt would result in financial hardship according to IRS standards. They also need to be current on all tax returns and cannot be in bankruptcy. Applying requires an application fee, which can be waived if you are a low-income taxpayer and an initial nonrefundable payment. Your debt will also still accrue interest while your application is reviewed.

Tax Help for Taxpayers with Back Taxes

Having unpaid back taxes can cause severe stress and dealing with the IRS on your own can be intimidating and time-consuming. A knowledgeable and experienced tax professional can help you understand your options better and do the heavy lifting when trying to get rid of your back taxes. Optima Tax Relief is the nation’s leading tax resolution firm with over $1 billion in resolved tax liabilities.

A new year could mean a financial fresh start. The IRS Fresh Start program was created to help struggling taxpayers and small businesses. In 2023, taxpayers are still asking how the program works. Here are some key details about the program.

The History of the Fresh Start Program

The Fresh Start Initiative was established in 2011 to give first-time tax offenders leniency and the opportunity to solve their tax issues through consolidated tax bills and payment arrangements. Shortly after launching the program, the IRS made it easier to remove federal tax liens. It also allowed taxpayers to come to more favorable payment arrangements with the IRS. One year after that, the IRS gave more taxpayers access to the Offer in Compromise (OIC) program.

Changes to Federal Tax Liens and Installment Agreements

The IRS used to file tax liens on balances above $5,000. The Fresh Start program increased the tax balance limit to $10,000. It also gave taxpayers the chance to withdraw their lien, which then helped those taxpayers access more credit.

Streamlined installment agreements (SLIAs) were also expanded in 2011 that allowed more favorable terms for the taxpayer and helped avoid tax liens. This allowed taxpayers with debt of up to $50,000 to be set up with a SLIA, up from the previous $25,000 cap. Further, the term length was increased from 60 months to 71 months. The simple installment agreement is preferred for most taxpayers since it does not require giving the IRS extensive documents detailing financial situations.

Changes to the OIC Program

The OIC program is very sought after by taxpayers with a large tax debt balance. An Offer in Compromise is essentially an agreement between the IRS and taxpayer that settles the owed tax debt for a lesser amount. However, offers are not accepted if the IRS thinks that the taxpayer is capable of paying the balance in full. In 2012, the IRS allowed greater access to the OIC program by revising how it calculates taxpayer future income, allowing taxpayers to repay student loans and past-due state and local taxes, expanding the allowable living expense amount, and reducing the offer amount for those who qualify for an OIC. It’s important to note that the IRS does not accept OICs often. In fact, the IRS only accepted about a third of OIC applications from 2010-2019.

Tax Help for Those Who Owe

The Fresh Start program can really help taxpayers who owe the IRS but don’t necessarily have the funds to pay their debt. Working with an experienced tax relief company can help ease the process. If you are wondering if you are eligible for the Fresh Start program, we can help. Optima Tax Relief is the nation’s leading tax resolution firm with over a decade of experience helping taxpayers.

Most people require assistance when it comes to preparing and filing a tax return. Some may even find themselves having to provide additional information to the IRS and do not know what it is or where to find it.

Hiring a tax professional could save individuals both time and money when dealing with the IRS. Tax professionals can also prepare tax returns, help file income taxes, and assist taxpayers when it comes to dealing with the IRS, tax notices, tax liabilities, audits, and more.

Types of Tax Professionals

There are various types of tax professionals who specialize in focused areas of tax relief or tax prep and carry specific professional licenses.

Certified public accountants or CPAs can provide a variety of services such as:

Maintaining financial records.

Examining financial statements.

Providing auditing services.

Preparing tax returns.

Some CPAs specialize in tax planning and preparation such as:

Tax audits.

Payment and collection issues.

Appeals.

Enrolled agents are trained to find federal tax matters and are licensed by the IRS. Enrolled agents can assist with the following:

The preparation of both individual and business tax returns.

The representation of clients.

Other aspects of being a tax professional.

A tax attorney is licensed by the state to practice law. Most states require an attorney to have a law degree and pass a test administered by the state (bar exam). Tax attorneys can assist taxpayer with:

The preparation of tax returns.

Tax planning.

Providing advice to clients on long-range strategies for reducing their taxes.

Like CPAs and EAs, tax attorneys have unlimited rights to represent a client before the IRS.

Areas of expertise

There are a range of services that tax professionals can provide to taxpayers that can help them understand their taxes better. Based on what service you need, choosing the right tax professional or tax preparer can help you get back on track with your taxes, small business, and much more.

Enrolled Agents are IRS-authorized tax professionals who work alongside the U.S. Department of the Treasury by providing representation to individuals who need tax assistance.

Certified Public Accountants (CPAs) have state certifications to practice accounting. These experts can help individuals navigate certain tax situations. CPAs are licensed to represent taxpayers before the IRS.

Retirement tax professionals can help individuals know how their retirement options will impact their taxes. These types of tax professionals have received advanced training in tax preparations specifically for retirement plan contributions, distributions, and rollovers.

Small Business/Sole Proprietor tax professionals specialize in working with small businesses’ tax returns and educate their clients on how to properly prepare both their personal and company returns. These types of tax professionals have specialized training in sole proprietors, partnerships, and S corporations.

Investment Income tax professionals specialize in big or small investments, and gains or losses. These tax professionals also show your current and future tax situations.

International Taxation tax professionals assist individuals who have lived or worked abroad. These tax professionals are trained in international taxation which includes, claiming foreign earned income exclusions, the foreign tax credit, or treaty benefits for nonresident aliens.

Professional Licenses

Enrolled Agents (EAs) and Certified Public Accountants (CPAs) are both experienced professionals who maintain high ethical standards. The main difference between an EA and CPA is that an EA specializes specifically in taxation. CPAs can provide a wider scope of tax services for individuals.

Working with an EA would be beneficial for those who have IRS issues such as individuals who are in collections or dealing with an audit with the IRS. An EA would be best suited for someone who needs assistance with the IRS to help them with their tax concerns. EAs are also a great option for those who need tax preparation assistance and planning advice for both individuals and businesses.

CPAs specialize in tax preparation that can help individuals identify both their credits and deductions that can help them qualify for an increase in their refund or help lower their tax bill. CPAs are also beneficial if someone needs their tax information compiled, reviewed, or audited.

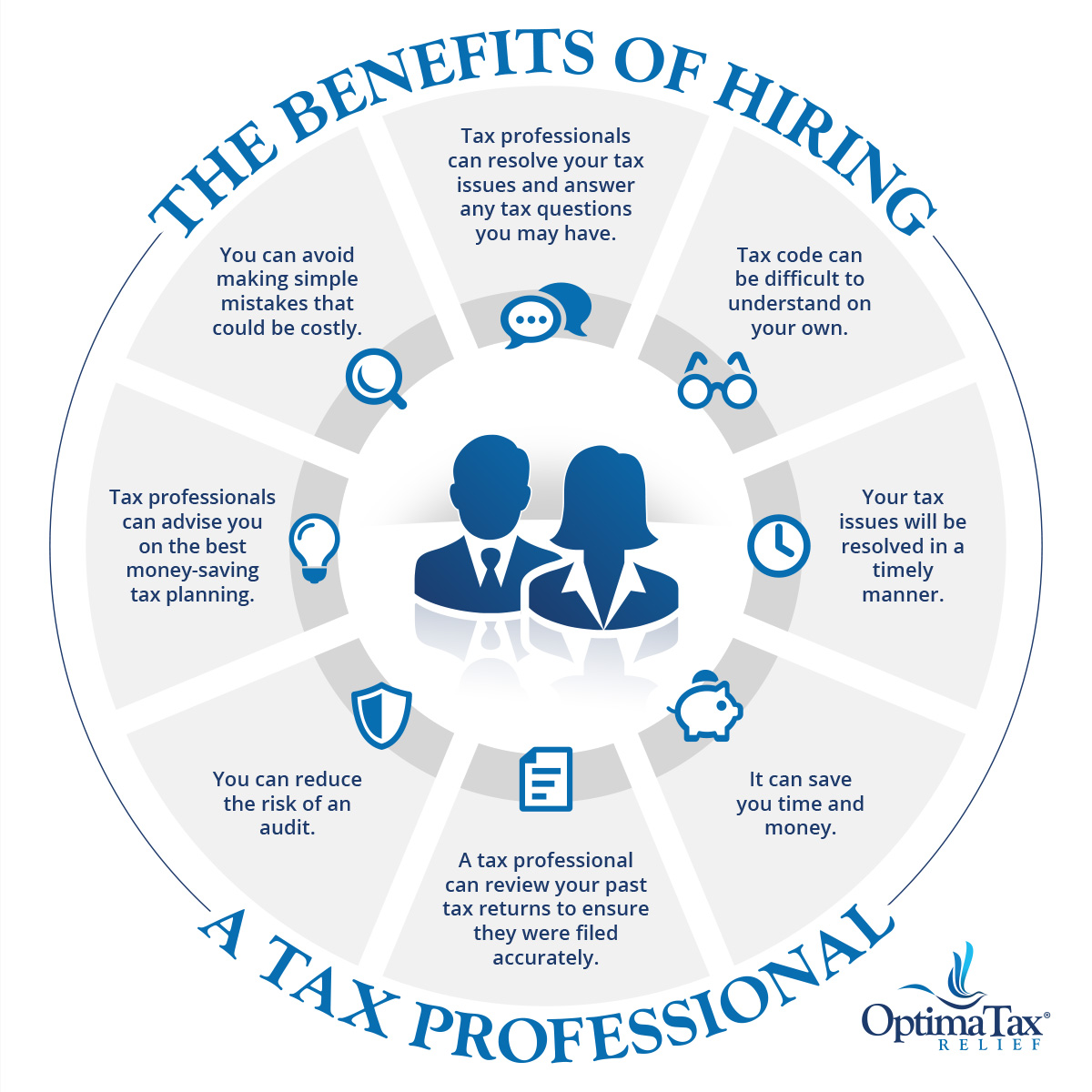

When should I hire a Tax Professional?

You should hire a tax professional if you are short on time, are unsure how to file your taxes correctly, or feel overwhelmed by IRS forms with preparing your taxes. Tax professionals can help answer tax questions that you may have and even resolve most tax issues you may have.

The tax code can be very complicated and if you are unsure on how to handle your tax matters, a tax professional can assist. For example, a tax professional can help reduce the risk of any audit and know how to deal with the IRS on your behalf if you do end up being audited. Tax professionals can also help taxpayers avoid making costly mistakes on their tax return such as missed deductions or triggering an IRS letter. Tax professionals can also review previous tax returns to see if there were any errors and needs to be amended.

How to find the right Tax Professional for you

Individuals searching for tax assistance should follow these steps in order to find a tax professional who best fits their needs:

Confirm your preparer has a tax identification number (ITIN).

Make sure to confirm tax fees to ensure you are not being overcharged.

Avoid tax preparers who do not e-file tax returns.

Make sure that your tax preparer signs their name and provides their Preparer Tax Identification Number (PTIN) on your tax return.

Make sure your tax professional can respond to the IRS. Enrolled agents, CPAs and attorneys that have a PTIN can represent you when it comes to IRS audits, payments, and collection issues.

10 Questions to ask a Tax Professional

Do you have an IRS-issued Preparer Tax Identification Number (PTIN)?

How do you keep up with the latest tax law? Are you regularly taking education courses?

Do you offer a free initial consultation?

Will you be the one preparing my return or someone in your office?

Do you offer IRS e-file, and will my tax return be submitted to the IRS electronically?

Will you keep my records and receipts on file? How long will you keep my records for?

When do you require payment?

When can I expect to receive my completed tax return?

What happens if I get audited?

Do you outsource your tax preparation?

Things to look out for when hiring a Tax Professional

Taxpayers should be aware of any red flags they experience when looking to hire a tax relief professional. Here is what individuals should look out for before hiring a tax professional:

Check the preparer’s qualifications.

Review the preparer’s history.

Ask about services and fees.

Make sure that the preparer offers e-filing.

Ensure your preparer has open availability if you have additional questions regarding your taxes.

Never sign a return if your preparer has added their name or PTIN.

How much does it cost to hire a Tax Professional?

The average cost of hiring a tax professional will depend on the complexity of the case that they are working on.

Consequences of not Hiring a Tax Professional

The federal tax penalties you could face by not hiring a tax professional to help you prepare your taxes could far outweigh the cost of soliciting tax help. Here are the repercussions individuals could face if they choose to not hire a tax professional:

Filing your own taxes could be time-consuming and confusing if you have never filed before.

You can miss out on tax preparation fees that could have been deductible.

You could miss out on certain credits or deductions if you are not aware of them.

If you get audited, you will not have a tax professional that can assist you through the process.

Filing your own taxes could lead to you making avoidable mistakes that could cause you problems with the IRS down the road.

Tax Relief Services at Optima Tax Relief

Optima Tax Relief offers tax relief services to individuals who are struggling with their IRS or state tax debt. Taxpayers that need assistance with tax preparation, setting up a payment plan with the IRS, getting out of collections, resolving an audit, or are looking to see if they qualify for a possible reduction in their total tax debt, should consider using Optima’s services.

Optima Tax Relief provides assistance to individuals struggling with unmanageable IRS tax burdens. To assess your tax situation and determine if you qualify for tax relief, contact us for a free consultation.

For taxpayers who have been working with the IRS, it is important for them to know that they have a right to finality. Specifically those who have had their tax return(s) audited by the IRS should know that there is a Taxpayer Bill of Rights in place to protect them.

For taxpayers currently in the audit process, here is what you need to know about your right to finality:

Taxpayers have the right to know

The maximum amount of time they have to challenge the IRS’s position.

The maximum amount of time the IRS has to audit a tax year or collect a tax debt.

When the IRS has finished an audit.

The IRS typically has three years from the date that a taxpayer files their return to review for an additional tax for the year in question.

There are very few exceptions when it comes to the three-year rule. An exception would be considered if a taxpayer fails to file a return or files a fraudulent return. In either case, the IRS would have an unlimited amount of time to assess tax for the tax years in question.

The IRS generally has 10 years from the date of assessment to collect unpaid taxes. It is important for a taxpayer to know that the 10-year period cannot be extended unless a taxpayer enters into a payment plan or the IRS obtains court judgments.

A 10-year collection period may be suspended when the IRS cannot collect money because a taxpayer has an ongoing bankruptcy or there’s a collection due process proceeding involving the taxpayer.

A taxpayer will only be subject to one audit per tax year. The IRS has the ability to reopen an audit for a previous tax year if the IRS deems it necessary.

If you need tax help, contact us for a free consultation.

The IRS is always prepared, shouldn’t you be as well? Do you need a tax relief lawyer?

Yes, absolutely.

This is a blog for a tax relief company with a small army of tax lawyers, so that’s what we’re paid to say, right? Well, yes, but it doesn’t make it any less true.

Benefits of Using a Tax Relief Lawyer: True Stories

A tax relief lawyer is a wise decision. In January, 2014, Forbes reported that Beanie Beans founder Ty Werner was convicted of evading $5.5 million dollars in taxes owed on the $27 million in interest accrued from millions of dollars stashed away in a Swiss bank account. The sentence? Two years on probation and some hefty fines, which were small change for a billionaire like Werner.

Unrelated, and a couple of months earlier, Daniel Thody, a defense contractor was found guilty to five counts of tax evasion for failing to report $15,000 and $50,000 in taxes from $1.8 million earned as a contractor for the Department of Defense. He faces up to 25 years in prison, 5 years for each count.

Which one do you think hired a tax relief lawyer and which one thought representing himself would be the smarter option? The old adage that he who represents himself has a fool for a client may be a cliché, but that doesn’t make it any less true either.

A tax attorney will ensure that you are treated better. It’s unfair, even illegal, but it’s also human nature. IRS agents are flesh and blood and if they can get away with bullying someone into their interpretation of the law, they probably will. A tax lawyer can ensure the IRS is playing by the rules and treating you fairly. IRS investigators are much more careful about asking inappropriate questions or wasting your time with unnecessary requirements if they know they are dealing with a tax attorney.

That was the finding of an investigation into nine groups in Ohio and Kentucky that sought nonprofit status. Organizations that didn’t have legal representation were more likely to have their applications stalled and receive inappropriate or unnecessary questions from the IRS.

You don’t have to worry about an IRS agent getting upset with you for hiring a tax relief lawyer either. The good ones prefer dealing with tax professionals because they don’t have to waste their time and patience explaining to you the ABCs of a tax audit or the basic IRS guidelines for a criminal investigation. In fact, hiring an experienced tax relief lawyer is generally seen as a sign of good faith to resolve your tax issues.

A few bad eggs may resent you hiring a lawyer and try to dissuade from doing so, but that’s when you really need a lawyer in your corner. The IRS’s own Declaration of Taxpayer Rights clearly states that “If you are in an interview and ask to consult such a person [a lawyer, agent or accountant], then we must stop and reschedule the interview in most cases.” Be suspicious if an IRS agent prefers not to deal with a tax professional.

Can the IRS See My Foreign Bank Account?

The IRS is a behemoth of an agency, one of the most powerful organizations on the planet. From 2008 through to 2014, over 50 bankers from Switzerland, India, Israel and other countries have been indicted for helping rich Americans squirrel billions of dollars into offshore accounts.

In 2013, the IRS also cracked the code of silence of Swiss financial institutions and got UBS, the largest Swiss Bank, to divulge confidential information on American tax evaders, and pay a $780 million penalty.

Even the IRS Thinks You Need a Tax Lawyer

The Taxpayer Advocate Service is an independent organization within the IRS which has the job of ensuring that you are treated fairly and helping you resolve problems with the IRS. Although it’s unlikely a Taxpayer Advocate Service lawyer will protect your interests quite as aggressively as a regular tax attorney, they are better than nothing, if you can’t afford to pay one.

If money is an issue, there is another option: Low Income Taxpayer Clinics. Although these clinics are partially funded by the IRS, they are completely independent and are operated by nonprofit organizations and academic institutions.

Only a Tax Attorney Can Represent You in a Criminal Investigation

Certified Public Accountants are great. When it comes to tax planning, business budgeting and asset management, a CPA is – all things being equal – more useful than a tax attorney is. But when you have a dispute with the IRS, especially if you’re accused of tax fraud or tax evasion, a tax relief lawyer is the only intelligent choice. Tax attorneys are the only ones who can represent you in a court of law and provide you the legal advice and analysis you need.

If that is not reason enough, I have two and a half words for you: attorney-client privilege. Unlike CPAs and accountants, attorneys cannot be subpoenaed to testify against a client in a criminal procedure.

Is it Worth it to Hire a Tax Attorney?

Does this mean you need a tax lawyer every time you get a letter from the IRS? No, of course not. You can probably deal with small mistakes and omissions by yourself or by giving your tax preparer a quick call. However, if there is any chance your case could go sour, you need to call a qualified and experienced tax attorney, and pronto. A good rule of thumb is that if you’re asking yourself whether it’s serious enough to merit calling a lawyer, it probably is.

A quick consultation call with a tax lawyer can save you thousands of dollars in unnecessary legal fees you could have avoided by not procrastinating. Tax lawyers know how IRS attorney think, many tax attorneys worked as IRS attorneys before hanging their own shingle. So, they know what to say, what not to say, and what buttons to push when negotiating your case.

Hiring a lawyer sends the IRS a clear and powerful message. You’re taking the investigation seriously; you’re not going to let IRS agents push you around; and you want to work with the IRS to avoid criminal charges.

The bottom line is that the IRS is scary enough when you have a first-rate lawyer at your side. So hire one already. Need to hire a tax relief lawyer? Our tax professionals at Optima Tax Relief are here to help.

The IRS Fresh Start Program Initiative, first announced, February, 2011, has had one goal: to make it easier for individuals and businesses to pay their back taxes and penalties. The Initiative has been expanded since then, but still holds true to its original purpose. How exactly will it affect you if you’re struggling to pay taxes? Here are the four components that Fresh Start Program has changed for your benefit.

What Is the IRS Fresh Start Program?

The IRS Fresh Start Program is a tax relief program that is designed to allow taxpayers to pay off substantial tax debts affordably over time.

Back in the bad old days, the image of the IRS was one of intimidation. Whether deliberately cultivated or not, the IRS did little to dispel this perception. In recent years, the IRS has sought to reboot the way it interacts with taxpayers, with agents receiving training and instruction in how to assist taxpayers who are in arrears rather than torment them. The IRS Fresh Start program combines penalty relief, installment payments; lien releases and a program known as Offer in Compromise that allows some taxpayers to settle their federal tax debts for less than what they actually owe.

How the IRS Fresh Start Program help waive Tax penalties

Originally, when paying and filing your taxes, missing the tax filing deadline meant immediate interest charges and penalties. But with the Fresh Start Initiative, qualifying unemployed taxpayers can apply to have Failure-to-Pay penalties waived for six months. This means that individuals have until October 15th, 2020 to pay their 2019 taxes.

How do you qualify for the IRS Fresh Start Program?

To qualify for the Fresh Start Program, you must:

Have been unemployed or seen a decrease in income

Earn less than $100,000 a year individually

Earn less than $200,000 a year as a couple

Not have a large tax balance from the previous tax year

The IRS Fresh Start Tax Relief program was launched in 2012 to help taxpayers who were struggling from the effects of the ongoing financial crisis. The first aspect of the program provided some unemployed taxpayers with exemption from the failure-to-pay penalty. Under this initial slice of the Fresh Start Initiative, taxpayers received a six-month reprieve from penalties on taxes owed for their 2011 federal tax returns. Although interest was still applied to any unpaid taxes, penalties were suspended from April 17 to October 15, 2012.

Easy Installment Agreements

The IRS Fresh Start Program also raised the maximum tax owed for taxpayers from $25,000 to $50,000 to qualify for streamlined repayment plans. Under the streamlined installment payment agreement program, taxpayers may establish payment plans online through the Online Payment Agreement page located on the IRS website. Taxpayers who owe more than $50,000 may still establish installment agreements but must either file a Collection Information Statement (Form 433-A or Form 433-F) or make sufficient payments against their past-due tax balance to bring the total tax owed below the $50,000 threshold.

How To Withdraw Notice Of Federal Tax Lien

The Fresh Start Initiative raises the minimum threshold for filing an IRS Notice of Federal Tax Lien on taxes owed from $5,000 to $10,000. The new standard is not retroactive, and the IRS may still impose liens against taxpayers who owe less than $10,000 when the agency deems that circumstances warrant doing so. To request that the IRS withdraw the Notice of Federal Tax Lien against liens that have been released, taxpayers must file Form 12777 – Application for Withdrawal, available on the IRS website. When citing a reason for the request, taxpayers should check the last box which states “the taxpayer, or the Taxpayer Advocate acting on behalf of the taxpayer, believes withdrawal is in the best interest of the taxpayer and the government.”

How To Make use of ‘Offer in Compromise’ and settle for less Tax

An Offer in Compromise, according to the IRS Fresh Start Program allows taxpayers to settle their obligations to the IRS for less than the total amount owed. The IRS only allows taxpayers to obtain relief under the Offer in Compromise program in circumstances where requiring repaying the full back taxes owed would constitute an undue burden or in cases where taxpayers demonstrate that they will be unlikely ever to be able to pay the full amount owed. Traditionally, the IRS has been stingy about accepting Offer in Compromise proposals from taxpayers; as a result, very few taxpayers were able to qualify for the program.

The IRS Fresh Start Initiative has established more flexible standards in evaluating the financial standpoint of taxpayers who request relief under an Offer in Compromise. As a result, more taxpayers may qualify. To be eligible for this IRS tax relief program under the Offer in Compromise program for grounds other than Doubt as to Liability, taxpayers must meet all of the following conditions.

Requirements to qualify for the Offer In Compromise program:

Cannot have an open personal or business bankruptcy petition

All required tax forms must have been filed

All required tax payments for the current year must be paid

Business owners with employees must have made current quarterly tax payments

An Offer in Compromise may be either for a single lump-sum payment or for installment payments. To request an Offer in Compromise, taxpayers must submit Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses along with either $205 to cover the application fee and either a payment of 20 percent of the proposed lump-sum payment or an amount equal to the first proposed monthly installment payment. Individuals and sole proprietors who qualify under Low Income Certification guidelines set by the IRS are exempted from paying the application fee.

New Installment Guidelines according to Fresh Start Program

Installment agreements allow a person to make monthly payments on their tax debt if they can’t afford to pay the total at once, and/or aren’t eligible for an Offer in Compromise. In the past, once an individual’s tax balance reached $25,000, the IRS began conducting a financial analysis of the person’s income and expenses to determine how much the taxpayer would pay per month. Additionally, a Notice of Federal Tax Liens was filed.

Under Fresh Start, more taxpayers will be able to avoid this invasive process altogether, as the tax balance threshold has been raised to $50,000. At that point, once the installment agreement process is started, you’ll now have six years to pay the debt off. If you are considering entering an installment agreement, let us know and we’ll make sure you qualify.

Notice of Federal Tax Liens and the Fresh Start Program

If an individual fails to pay their tax debt the government can file a claim against that person’s property with a federal tax lien. “Property” includes everything an individual owns, including real estate, vehicles and financial assets. The Notice of Federal Tax Lien alerts creditors that the government has a legal right to a taxpayer’s property. This may limit your ability to get credit.

Similar to installment agreements, FSI has raised the Notice of Federal Tax Lien filing threshold to $10,000 from $5,000. The IRS might still choose to file at an amount less than $10,000, but it’s not as automatic as before.

How the IRS Fresh Start Program can help with your Tax problems

While none of these alternatives represents an easy tax solution, each of them does provide a viable avenue for tax relief. If you have been struggling to pay your federal income tax burden, investigating possible assistance under the IRS Fresh Start Tax Relief program is definitely worth your while, either on your own or with the assistance of a tax professional. You may find that your overall tax burden is significantly reduced.

Wondering if you’re eligible for the Fresh Start program? Give us a call.

Do you need tax relief help? If you’re struggling with paying your taxes, don’t know how to fill out an Offer in Compromise or don’t know which forms to file, contact us today. We’ll help you take advantage of the Fresh Start Initiative, and deal with the IRS so you don’t have to.

[tagline_box link=”/get-tax-help” button=”Get Tax Help” title=”Let Optima Tax Relief Help” description=”Our professionals will put your mind at ease.”][/tagline_box]